Litigation finance is growing in prominence in the legal industry, embraced not just by lawyers but also increasingly by courts and state bars. As lawyers and claimholders have come to understand the utility and flexibility of litigation finance, the demand for funding has increased, and so too has the number of funders in the market. Some funders (like Lake Whillans) focus exclusively on litigation financing, whereas others are incorporating litigation finance investments as part of a larger investment portfolio. Some funders are interested only in the highest-value disputes, whereas others target smaller investments. Some will fund a strong case in any area of commercial litigation, whereas others specialize in a more focused range of cases.

How are claimholders choosing among the increasing diversity of funding options? How should they be choosing? In this article we first present some empirical evidence on considerations in funder selection and then offer our advice, gleaned from our long experience in the litigation finance market.

How are claimholders choosing a funder?

You might expect a claimholder who is new to litigation finance to begin with rankings such as those produced by Chambers & Partners. (Lake Whillans as a firm, and Lake Whillans co-founder Boaz Weinstein individually, each have been ranked among the top bands in every year that the Chambers rankings have been produced.) But although rankings may be the starting point, the primary factor in the ultimate decision is not which funder has the strongest reputation. Rather, lawyers report that the most important consideration is which funder offers the most favorable economic terms.

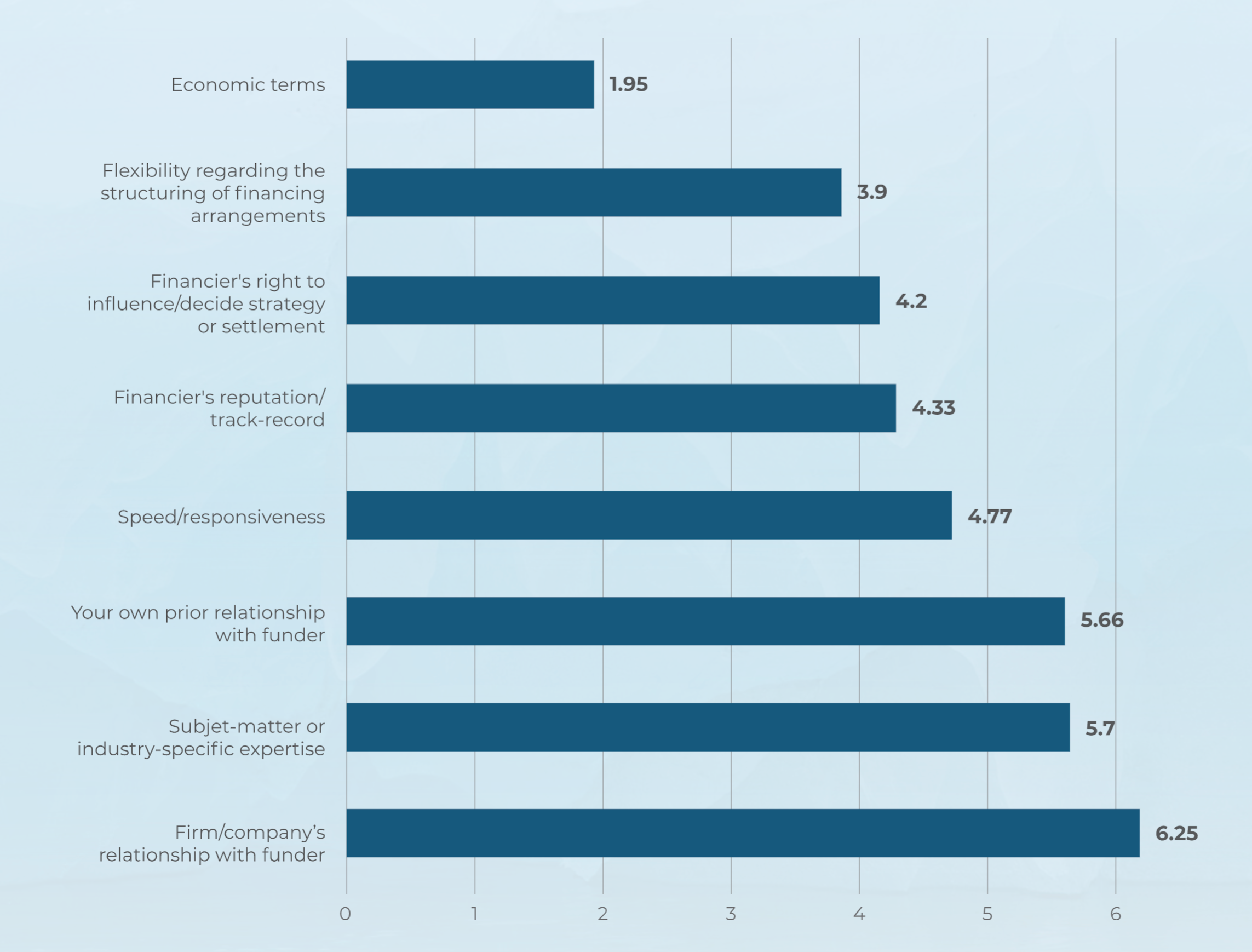

Lake Whillans and Above the Law conduct an annual survey of lawyers—both at law firms and in-house—to understand their perspective on litigation finance. In our 2021 edition, we asked respondents to rank eight factors in choosing a litigation funder, with “1” as most important and “8” as least important. Here are the results:

Partners and in-house counsel both identified economic terms as the most important consideration, but partners ascribed this factor greater relative importance, scoring it 1.77 as compared to 2.08 for in-house counsel. Both groups ordered their priorities nearly identically.

It isn’t surprising that the cost of capital is an important factor. After all, the headline cost figure is one of the simplest ways to compare across funders. But savvy claimholders and counsel understand that alignment on other dimensions besides cost is also critically important. In the next section we propose a more comprehensive set of factors to consider when deciding which funder(s) to approach.

What factors should claimholders and counsel consider in evaluating funders?

Preferred Investment Type. Funders vary in the types of cases they invest in, both with respect to claim type and forum, and may exclude certain types of claims. Lake Whillans invests in most commercial cases, including breaches of contract, breaches of fiduciary duty, business torts, trade secret misappropriation, antitrust, and investor-state disputes. We do not fund patent claims. We invest in single cases as well as portfolios (including law firm portfolios). We will fund litigation or arbitration pending in the U.S. or Canada, as well as international arbitration.

Preferred Investment Size. Funders often have a minimum and maximum investment size. Our typical investment ranges from $1.5-$10 million for single cases, and larger amounts for portfolios. (We are willing to consider investments of smaller or larger amounts under the right circumstances.) The size of the investment we are willing to make depends on the quantum of damages, likely settlement scenarios, the current posture of the matter, and other factors. Understanding your capital needs before you approach a funder can help you find the right one.

Required Risk Allocation Between Funder, Claimholder, and Counsel. Some funders prefer not to bear all the risk of the litigation and require the claimholder and counsel to “take risk.” For the claimholder, that means using its own capital to pay at least some portion of the fees and expenses. For counsel, it means taking a contingent stake (i.e., upon success, the firm earns a percentage of the proceeds, fixed fee, or multiple on unrealized fees) in lieu of some portion of its ongoing fees. Distributing the risk this way may not be feasible or desirable for every claimholder or its counsel, so it’s important to understand if risk-sharing is among a funder’s requirements. (While we are open to transactions that involve risk-sharing, Lake Whillans does not require it.)

Reserved Capital. Litigation can take several years so you will want to be sure that the financier is able to make good on its commitments in the future. Ask whether the funder currently has sufficient committed capital to fully fund the investment? What percentage of the budget will the funder hold in reserve? (Lake Whillans reserves 100% of its committed investment amounts.)

Right to Exit Funding. Speaking of getting to the finish line with resources in place, you should understand whether and under what conditions the funder can stop funding the litigation. For example, some funders may contract for a right to exit if there is a material negative change in the litigation (negative discovery, adverse ruling, etc.). These terms can leave the claimholder and counsel in a difficult place. In general, we underwrite our investments with those risks in mind and commit to funding cases to final resolution as defined for the particular investment.

Control Over Litigation or Settlement. Some funders may contract for direct or indirect control over the litigation or settlement. For example, while a funder may not have the authority to accept or deny a settlement offer, there may be terms that increase the cost of the funding if offers deemed reasonable by the funder are rejected. (Lake Whillans does not include provisions of this sort in its funding contracts.)

Other Points of Comparison. There are other differentiators that may be relevant in choosing among funders. Some examples include whether the funder requires exclusivity while it’s conducting diligence (Lake Whillans does not), the speed at which a funder can arrive at a decision (we generally conduct our diligence within 30-45 days after reaching agreement on the economic terms), the funder’s experience with the transaction type and with the subject matter, and the funder’s flexibility in structuring the deal to meet the needs of the claimholder and its counsel.

Personal Compatibility. Finally, it’s important to find the “right fit” when partnering with a funder. Size up potential funders during the first few discussions to decide whether you trust the people on the other end to be constructive partners through the ups and downs of litigation. One thing to consider in this regard is whether the funding team has experience with cases like yours. Funders who have been involved with similar cases can be a helpful sounding board over the course of the litigation. At the same time, you’ll want to avoid funders who seem too eager to insert themselves in litigation strategy. Try to feel out a funder’s typical approach to communication with counsel over the course of a case to ensure that expectations are aligned.

* * *

Applying a relatively short list of criteria, it’s possible to choose efficiently the right funder(s) to approach for your matter. We’ve created this spreadsheet to help keep track of your options, which we hope you will find useful. We also encourage you to contact us to discuss our approach, the industry or specific opportunities.